Home » Pain and Suffering After a Car Accident: How Much Is Your Case Really Worth?

When you’ve been in a crash, the bills are at least visible — ER visits, MRIs, physical therapy, missed paychecks.

Pain and suffering is the opposite. You feel it every day, but you can’t hold it in your hands… and that makes it very easy for an insurance company to undervalue or ignore.

This guide is your deep dive into how pain and suffering is treated in car accident cases, what really affects the value, and how 833-GET-PAID approaches “What is my case worth?” under your state’s laws.

Quick note: This article is general information, not legal advice. Every case is different, and only a lawyer licensed in your state can tell you how your specific facts and laws interact.

Understand what “pain and suffering” actually covers. It’s a category of non-economic damages that includes your physical pain, emotional distress, trauma, sleep problems, anxiety, loss of enjoyment of life, and more — not just “being sore.”

See why there’s no real “average” pain and suffering payout. Law firms and insurers agree there is no meaningful universal “average settlement” for pain and suffering because every case is different and non-economic damages are highly fact-specific.

Learn the two main ways insurers and lawyers try to put a number on your suffering. Most sources describe two common methods: the multiplier method, which multiplies your medical bills and other economic losses by a number (often 1.5–5+), and the per diem method, which assigns a daily rate to your suffering for a period of time.

Spot the real-world factors that drive pain and suffering up or down. Injury severity, how long you’re in treatment, permanent limitations, impact on work and daily life, mental health, fault disputes, policy limits, and state damage caps all matter.

Learn how to document your pain so insurers can’t pretend it doesn’t exist. Medical records, photos, a simple daily pain journal, mental-health notes, and statements from family or coworkers can dramatically strengthen the value of your non-economic damages.

n a car accident claim, most of your compensation falls into two big buckets:

Economic damages:

Money you can prove with a bill, receipt, or paystub:

Medical bills (ER, imaging, surgery, therapy)

Future medical expenses

Lost wages and lost earning capacity

Property damage (e.g., your car)

Non-economic damages (pain and suffering):

Harms that are real but don’t arrive with a price tag:

Physical pain and discomfort

Emotional distress and mental anguish

Anxiety, depression, PTSD symptoms

Loss of enjoyment of life (activities you can’t do anymore)

Scarring, disfigurement, embarrassment

In some states, loss of consortium for your spouse/family

Most states allow car accident victims to claim both economic and non-economic damages when someone else’s negligence caused the crash, although how that works can differ based on things like no-fault rules and comparative negligence.

Big picture: Economic damages compensate you for financial losses.

Pain and suffering compensates you for how the injury changed your life.

A simple way to visualize it:

| Type of Damages | Examples | How It's Measured |

|---|---|---|

| Economic | ER bill, MRI invoice, missed paychecks, car repair | Bills, statements, wage records |

| Non-Economic (P&S) | Pain, nightmares, fear of driving, lost hobbies | Jury/negotiation judgement based on proof |

Courts and insurers break pain and suffering into a few overlapping categories. You don’t have to use these labels yourself — but it helps you recognize that what you’re feeling does count.

Physical pain and discomfort

Ongoing pain in your neck, back, or joints

Headaches or migraines

Pain from surgery, injections, or other procedures

Nerve pain, burning sensations, and limited range of motion

Long-term or permanent pain after serious injuries

Emotional and mental suffering

Anxiety, panic attacks, or constant worry

Depression or hopelessness after the crash

PTSD symptoms: flashbacks, intrusive thoughts, exaggerated startle response

Sleep problems or nightmares

Fear of driving, riding in a car, or returning to the crash location

Loss of enjoyment of life

Giving up hobbies (sports, working out, dancing, etc.)

Missing out on vacations, family events, or important milestones

Not being able to play with your kids the way you did before

Disfigurement, scarring, and embarrassment

Visible scars or deformities

Self-consciousness in social or professional settings

Feeling “permanently changed” by the crash

In some states, a spouse or close family member might also seek loss of consortium, which covers the impact on the relationship: loss of companionship, intimacy, and shared activities.

If you’ve Googled this topic, you’ve probably seen numbers all over the place:

Some sources mention “typical” personal injury settlements around the tens of thousands of dollars, often citing consumer legal surveys.

Some law firms say many moderate-injury cases land in the low five-figure range, while serious and catastrophic cases can reach six or seven figures.

Some even quote “average car accident settlements” in specific cities or states.

Here’s the problem:

There is no real “average” pain and suffering settlement that applies to everyone.

Multiple firms and legal resources explicitly say there’s no meaningful average for pain and suffering, because every accident, injury, and jurisdiction is different.

“Average” numbers are pulled from mixed groups of:

Minor soft-tissue injuries

Serious fractures requiring surgery

Catastrophic spinal cord or brain injuries

Cases where pain and suffering was small or extremely high

So if you see a generic figure like “the average settlement is $X,” remember:

That number includes people whose experiences look nothing like yours.

A crash that leaves you with months of therapy and a permanent limp should not be valued like a minor fender-bender — but raw averages can blur that difference.

What is helpful about national or regional data?

It shows that injury cases generally settle for more than property-damage-only claims, often significantly more.

It suggests a wide spread:

Many moderate cases end under $25,000–$50,000, while more serious injuries often exceed that.

A small slice of catastrophic cases account for very large settlements or verdicts.

But these numbers don’t know:

Your exact injuries and prognosis

How long you’ll need treatment

How your state handles non-economic damages or any caps

Whether the at-fault driver has low policy limits

Whether you have a strong, well-documented pain story

That’s why firms like Crash Advocate stress that case-specific evaluations by a lawyer in your state are the only honest way to answer “What is my case worth?”

Each attorney in the Crash Advocate network will use their own professional judgment, but many lawyers think about pain and suffering in levels rather than a single “average.”

A simplified way of thinking about it:

Level 1 – Short-term injuries

Soft-tissue injuries (whiplash, sprain/strain)

A few weeks or months of treatment

No surgery, full recovery expected

Level 2 – Moderate injuries

Fractures, herniated discs, or longer therapy

Pain lasting several months or more

Possible temporary work restrictions

Level 3 – Serious injuries

Surgery, hardware (plates/screws), long-term limitations

Ongoing pain, life activities permanently altered

Psychiatric impact (PTSD, serious depression)

Level 4 – Catastrophic injuries

Traumatic brain injury, spinal cord damage, major burns, amputations

Permanent disability, need for assistance with daily tasks

Massive impact on family, work, and future plans

Each level doesn’t guarantee a number — it simply helps your attorney frame how severe your pain and suffering really is, and whether a one-size-fits-all formula is fair or wildly off.

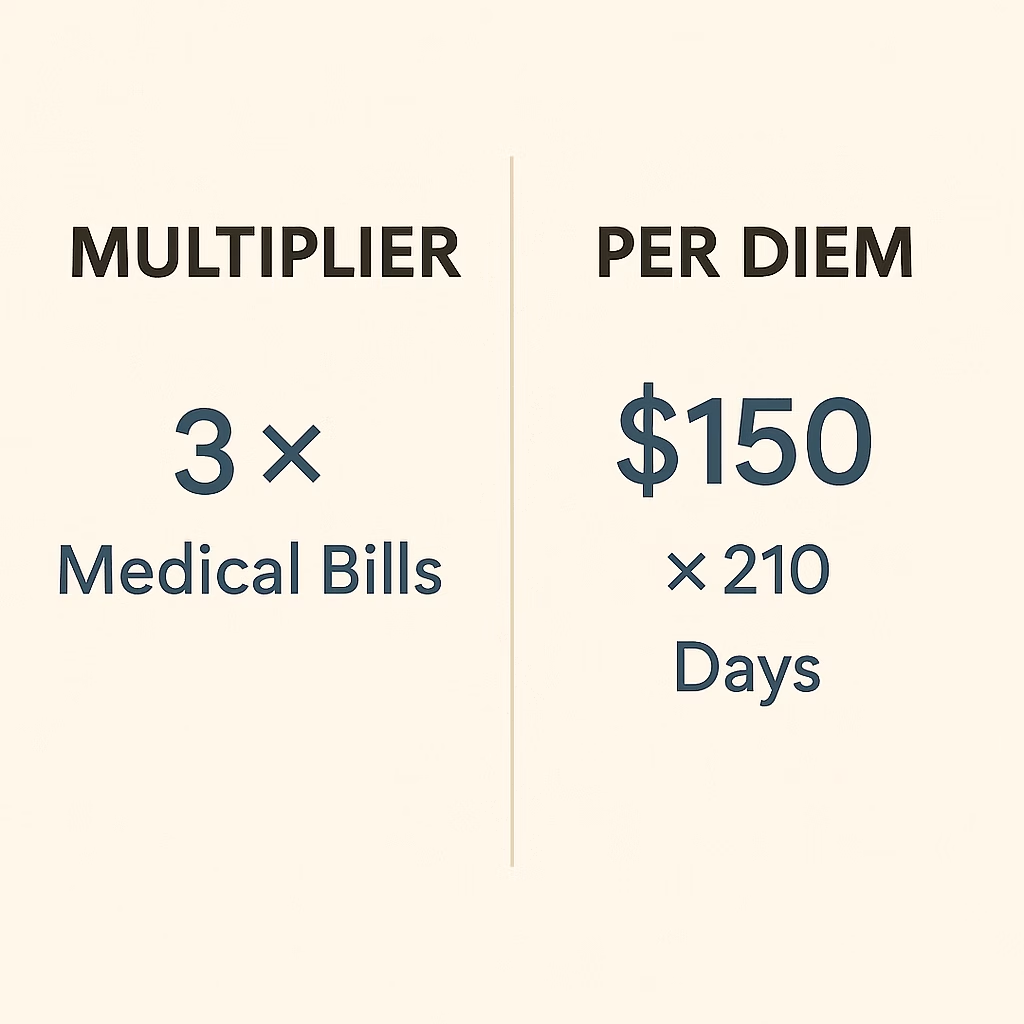

The multiplier method is the approach most people hear about first:

(Economic damages) × (multiplier) = estimated total damages

Where:

Economic damages = your medical bills + lost wages + other financial losses

Multiplier = a number like 1.5, 2, 3, 4, or more, chosen based on:

Injury severity

Length and type of treatment

Permanent limitations or disfigurement

Emotional impact

Clarity of fault

How credible and well-documented your claim appears

Example (just for illustration, not a promise):

Medical bills and lost wages total: $40,000

Insurer argues for 1.5× multiplier:

$40,000 × 1.5 = $60,000 (includes pain and suffering)

Your lawyer argues for 3× multiplier:

$40,000 × 3 = $120,000

Both sides are looking at the same bills — the disagreement is largely over the multiplier, which is where your pain and suffering lives.

Some law firm and legal-education sources note that in more serious cases, fair multipliers can exceed 5, especially where there’s permanent impairment or significant emotional trauma, though insurers often resist those numbers.

The per diem (per day) method does it differently:

Reasonable daily rate × number of days you reasonably suffered

Steps:

Choose a daily rate (often based on a person’s daily earnings, or some reasonable substitute).

Multiply by the number of days from the crash until:

You reached maximum medical improvement, or

Your pain and restrictions eased significantly

Example:

Daily rate: $200

Days of significant pain and limitations: 105 days

$200 × 105 = $21,000 as a starting point for pain and suffering discussions

Limitations:

Awkward for people who were unemployed, students, or retired at the time of the crash.

Hard to apply in cases where pain continues indefinitely — how many days should be counted?

Like the multiplier method, it’s not a binding legal rule, just a way to frame negotiations.

A few key realities:

Juries aren’t required to use either formula.

They’re usually told to award a “fair and reasonable” amount based on the evidence and their common sense.

Insurers lean heavily on software and internal calculators.

Companies like State Farm and others use computer systems that assign values to certain injury codes and treatment patterns; multiple legal sources say these tools often produce lowball pain and suffering ranges.

The same case can look very different to a jury than it does to an adjuster.

Firms that track verdicts report situations where an insurer’s calculator suggested one number, but the jury ultimately awarded several times that amount in non-economic damages.

Because of all this, many experienced attorneys treat multipliers and per diem calculations as:

A starting point for negotiation, and

A way to help a jury “reverse engineer” why a requested amount is reasonable — not a rigid rule.

Even when two people have similar medical bills, their pain and suffering values can be worlds apart. Here are the biggest drivers.

Generally, the more serious the injury and the longer the recovery, the higher the potential pain and suffering.

Short-term soft-tissue injuries:

A few weeks of sore muscles and physical therapy will usually generate less pain and suffering exposure than…

Fractures or disc injuries:

Broken bones, herniated discs, or injuries requiring injections or surgery tend to support higher non-economic awards, especially when pain continues even after treatment.

Permanent impairment:

If your injury leaves you with long-term restrictions, chronic pain, or an inability to return to your old job, that can multiply the perceived severity of your suffering.

Importantly, consistent medical treatment matters. Gaps in treatment or no-shows for appointments give insurers ammunition to argue that your pain wasn’t that bad.

Insurers and juries pay attention to the human story:

Can you still pick up your child or grandchild?

Can you stand all day at work?

Can you exercise, hike, or play your sport?

Can you sleep through the night without pain or nightmares?

Specific examples (“I had to quit my weekend softball league” or “I can’t lift more than 10 pounds now, which changed my job”) are more persuasive than general statements like “it hurts a lot.”

Car accident victims commonly experience:

Fear of driving, riding as a passenger, or being near traffic

Intrusive memories or flashbacks

Irritability, anger, or emotional numbness

Panic attacks or intense anxiety

Depression and withdrawal from activities they used to enjoy

Mental health professionals can diagnose conditions like PTSD, adjustment disorders, or major depressive episodes, and their records and testimony can significantly increase the documented value of pain and suffering.

Getting help is important for your recovery and for proving the emotional side of your claim.

Two cases with identical injuries can still end up with very different pain and suffering outcomes because of legal limits.

Damage caps

Some states cap non-economic damages in certain types of cases, particularly medical malpractice. Others have broader caps that can affect personal injury awards more generally.

These caps can limit what a jury may award regardless of the severity of your suffering.

Insurance policy limits

If the at-fault driver has only the minimum required liability coverage, their insurer usually won’t pay more than that limit, even if your pain and suffering is worth more.

Comparative negligence and no-fault rules

In comparative negligence states, your compensation can be reduced if you’re found partially at fault (for example, 20% at fault could reduce your total recovery by 20%). Some states cut off recovery entirely if you’re 50% or 51% at fault.

In no-fault states, you may need to meet a “serious injury” threshold before you can even seek pain and suffering from the at-fault driver.

Because these rules vary widely, 833-GET-PAID works with lawyers licensed in the states where they practice, who know the local caps, thresholds, and jury tendencies.

Pain and suffering is subjective, but it shouldn’t be mysterious. The more concrete evidence you have, the harder it is for an adjuster to brush off your experience.

Common proof includes:

Medical records and doctor notes

Diagnoses, test results, physical exam findings, and your reported symptoms over time.

Treatment timeline

Consistent follow-up visits, referrals to specialists, physical therapy, injections, surgery — all show ongoing pain and effort to get better.

Mental-health records

Notes from counselors, psychologists, or psychiatrists addressing anxiety, depression, PTSD, and their impact on daily life.

Photos and videos

Images of bruising, swelling, surgical scars, braces, casts, and mobility aids; video of how you move, walk, or climb stairs.

Witness statements

Family, friends, and coworkers can describe changes in your behavior, mood, energy, and abilities since the crash.

A good attorney takes all of this and builds a narrative: “Here’s how this crash has changed this person’s life.”

You don’t need anything fancy. A notebook, spreadsheet, or app works.

Each day (or every few days), note:

Your pain level (0–10 scale) and where it hurts

What activities you couldn’t do or needed help with

How you slept

Any emotional symptoms (panic, crying spells, numbness, irritability)

Medications you took and side effects

Missed events (work days, social events, kids’ activities)

Over weeks and months, this creates a powerful picture of your suffering. Lawyers and some legal guides regularly recommend these journals because they give jurors and adjusters something concrete to understand.

Many firms can provide simple templates for clients to use.

Insurers are absolutely watching for anything they can twist.

Social media:

Even a carefully cropped “good day” photo, or a trip where you needed help to get through, can be used to argue “Look, they’re fine.”

Exaggeration:

If your story doesn’t match your medical records or surveillance footage, it can seriously hurt your credibility.

Talking too freely to the adjuster:

Casual statements like “I’m feeling better” or “it was just a little fender-bender” can be used to argue your pain and suffering is minimal.

833-GET-PAID’s own car accident guide warns about adjuster tactics and emphasizes controlling communication with insurers — one reason they encourage people to call 833-GET-PAID before giving detailed statements.

It’s time to be very cautious — and probably talk to a lawyer — if:

You get a quick settlement offer in the days or weeks after the crash, before anyone really understands your injuries.

The adjuster insists your pain is “just soreness” and tries to close the claim while you’re still treating.

You’re asked for a recorded statement and detailed medical history before they’ve even accepted fault.

You feel pressured to sign broad medical authorizations that let them dig through years of unrelated records.

These are classic moves to minimize both your economic and non-economic damages — especially pain and suffering.

833-GET-PAID is a national marketing network that connects accident victims with experienced personal injury attorneys across the U.S.

Lawyers in that network typically:

Investigate the crash and gather evidence

Police reports, witness statements, photos, video, and any available electronic data.

Collect and analyze your medical and mental-health records

To understand the full scope of your physical and emotional injuries.

Calculate and negotiate your pain and suffering

Using both:

Traditional tools (multiplier/per diem methods, national and local verdict data), and

Human judgment about how your story will resonate with a jury.

Handle insurance communications and settlement talks

So you’re not the one arguing with adjusters or worrying about saying the wrong thing.

File a lawsuit when necessary

Particularly when an insurer’s software-driven offer doesn’t even come close to your documented pain and suffering.

Money pressure is one of the big reasons people accept lowball offers.

That doesn’t mean:

Everyone qualifies, or

You should automatically take lawsuit funding (it can be expensive)

But it does mean:

You may have options other than “take whatever the insurer offers” vs “go broke while you wait,” which can directly affect your ability to hold out for fair pain and suffering compensation.

Specific funding structures and availability vary by state, case type, and partner; you’d need to ask your assigned attorney what’s realistic in your situation.

Most insurers start with your medical bills and other economic losses, then use internal software or a “multiplier” (often somewhere between 1.5 and 5) to estimate non-economic damages based on factors like injury severity, recovery time, and daily-life impact. That number is a negotiation starting point, not a legal rule.

No meaningful universal “average” exists. Multiple legal resources say there’s no true average pain and suffering settlement because every accident, injury, and jurisdiction is different. National surveys show typical personal injury awards clustered around the low tens of thousands of dollars, but those figures combine minor and catastrophic cases and don’t predict any one person’s result.

Pain and suffering is usually higher when injuries are severe or permanent, treatment is long and intensive, emotional distress is clearly documented, daily activities and work are significantly affected, fault is clear, and there’s strong, consistent medical and witness evidence supporting your story.

Yes. Some states cap non-economic damages in certain cases, and every case is practically constrained by the at-fault driver’s insurance policy limits unless there are additional defendants or coverage. Comparative negligence and no-fault rules can also limit or reduce pain and suffering recovery based on your state’s specific laws.

You can negotiate with an insurer on your own, but their systems and training are designed to minimize non-economic payouts. Lawyers who handle car accident cases every day know how to document your pain, attack lowball calculator outputs, and present your story in a way that persuades adjusters — and, if necessary, juries — to award full and fair pain and suffering damages.